Home Loan Part Payment Calculator in Excel helps you to plan your home loan repayments to close your loan before time and save interest amount to be paid on the home loan taken by you.

While making home loan part payment, you have 2 options – either to reduce EMI or tenure. It is best to reduce the tenure since you will be paying less interest amount compared to going with reducing of EMI. We will check this with help of examples below. Also it is important to note that the interest component in EMI is high at the initial stages of home loan. So it is best to make home loan part payment or prepayment at the initial stages of the loan (within 2-4 years after starting home loan EMI).

Let us understand home loan part payment or prepayment in more details.

HOME LOAN PART PAYMENT CALCULATOR EXCEL VIDEO

Watch more Videos on YouTube Channel

As seen in above video, we have 2 options while make home loan part payments or prepayments, and reducing tenure will save us more interest amount compared to reducing EMI option.

Let us now understand the home loan components.

HOME LOAN EMI COMPONENTS

- When you apply for home loan to buy a new house or buying a resale property your EMI is calculated using this Home Loan EMI Calculator

- In this Home Loan EMI, there are two components – Principal Amount and Interest Amount

- Principal amount is the amount that you have taken as home loan and have to pay back to the bank or financial institution from where you have taken loan

- Interest amount is the interest you have to pay every month based on the home loan interest rate, which becomes the profit of the bank

- This interest amount is high initially due to your loan balance being high at the initial stages of the loan repayment tenure

- The interest amount decreases with the decrease in the remaining balance of your loan amount. In this way, maximum interest amount is taken by you during the initial stages of your loan repayment tenure

- The principal amount component is low during the start and increases with time as you pay your home loan EMI

- Hence you can make part payment during the initial stages of your home loan to save maximum interest amounts

ALSO READ: Home Loan Mistakes you should avoid

HOW INTEREST IS CALCULATED IN HOME LOAN EMI

Interest on your home loan is calculated based on the interest rate and the remaining balance in your loan account.

Let us understand this with example:

Loan amount = Rs. 30 Lakh

Interest rate = 9.5% (annual interest rate)

Tenure = 20 years

Calculated EMI will be Rs. 27,964As seen above, Rs. 27,964 will be the home loan EMI for above given example. Let us calculate the interest amount component from this EMI amount for the first month when loan balance is Rs. 30 Lakh using below formula:

Interest amount = monthly interest rate * Loan Balance / 100

Interest amount = (9.5% / 12) * Rs. 30,00,000 / 100

Interest amount = 0.79% * Rs. 30,00,000 / 100

Interest amount = Rs. 23,750So the interest amount from first month EMI will be Rs. 23,750, out of the Rs. 27,964 EMI amount that you pay in the first month. That is a very high amount of interest you pay!

The remaining amount in EMI, that is Rs. 4214 ( Rs. 27,964 – Rs. 23,750) will be your principal amount from your EMI in the first month. This principal amount will be reduced from your loan balance and the interest will be calculated accordingly in the second month using this updated loan balance amount.

ALSO READ: Home loan with Variable Interest Rate

HOW TO SAVE HOME LOAN INTEREST COMPONENT

You can save home loan interest amount by making part payments.

Home loan part payment or prepayment is the process of depositing amount against your existing loan balance, which will reduce the balance based on your deposit amount and thus help you to save the interest component in your upcoming home loan EMIs.

As mentioned previously, part payments or prepayments can be made during the initial stages of the home loan to save more interest amounts.

While making part payments, you have the option to reduce EMI or tenure.

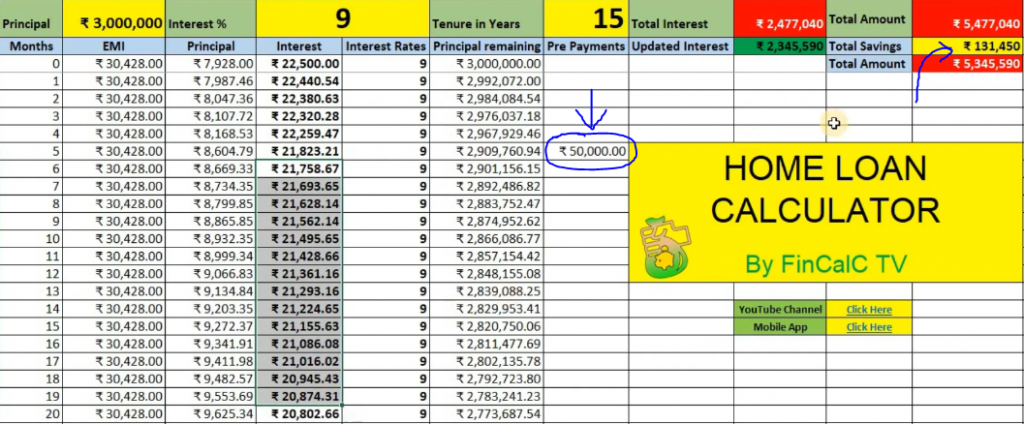

Below is the example with reducing tenure after loan part payment:

As seen, we save Rs. 1.31 lakh when reducing tenure just by making part payment of Rs. 50,000 in 6th month of the home loan tenure.

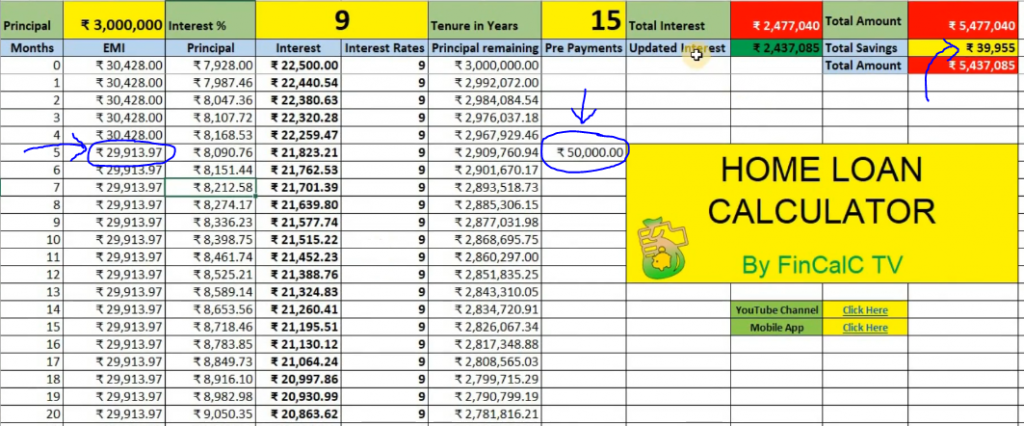

Let us compare this saving when we reduce the EMI amount after part payment:

So we only save Rs. 39,955 while we reduce the EMI amount after making same part payment of Rs. 50,000 after 6th month of the loan tenure start.

This proves that reducing tenure is better compared to reducing EMI while making home loan part payment or prepayment.

Let us answer few important questions on home loan part payment.

Is it good to pay part payment in a home loan?

Yes, home loan part payment or prepayment helps to save interest amounts in home loan.

Are there any charges for part payment of home loan?

Part payment charges are applicable for fixed interest rate home loan. But for variable interest rate home loan, that are no part payment or prepayment charges applied.

Does EMI reduce after part payment?

You have the option to reduce EMI after making part payment. So if you cannot afford the mentioned EMI, you can reduce the EMI after making part payment, but we have seen above that reducing tenure will help you save more interest amount after making part payments.

DOWNLOAD HOME LOAN PART PAYMENT CALCULATOR IN EXCEL

Fill below form to download the home loan part payment calculator in excel. This can help you to plan the home loan EMI payments and close the home loan before time by making prepayments regularly:

CONCLUSION

While home loan EMI can be paid consistently throughout the tenure of the home loan, it is best to make home loan part payment to reduce the principal outstanding balance in your loan account.

Reducing tenure while making part payments will help you save more interest amount compared to reducing EMI with same amount of prepayment. Also, reducing tenure will help you to pay the EMI for less number of months.

0 Comments