Equity Mutual Funds Taxation is simple to understand where short term capital gains are taxed at flat 15% irrespective of the income tax bracket you belong to, and long term capital gains are taxed at 10% on the profits made above Rs. 1 Lakh in a financial year. Short Term Capital Gains (STCG) are the profits you make from equity mutual fund units after holding them for less than 1 year, and Long Term Capital Gains (LTCG) in equity mutual funds are the profits you make after holding them for more than 1 year.

Let us understand Equity Mutual Funds Taxation with Examples.

WHAT IS EQUITY MUTUAL FUNDS?

- Equity Mutual Funds are the type of mutual funds that invest at least 65% of the total assets in equities or stocks

- The remaining amount can be invested in debt or money market instruments to fulfill the need of redemptions made by investors

- Equity Mutual Funds are risky in nature since they invest in stocks of companies. this risk is directly proportional to the amount of money allocated to equities of companies. But over long term, equity mutual funds are known to give good returns

- Mutual Fund with 90% allocation to equities (stocks) will be more risky compared to the mutual fund with 65% of allocation to equities in their portfolio

- Mutual funds are allocated with fund manager to select equities or stocks of companies to maximize returns on your investments

- Every mutual fund has an associated cost called as expense ratio, which is capped at 2.5% by SEBI. This expense ratio is the cost of handling your invested amount by fund manager and team, to maximize your returns on invested amount

- Expense ratio of funds that buy and sell more frequently will have high expense ratio compared to other funds that buy and sell less frequently while holding the stocks for long period

ALSO READ: Direct vs Regular Mutual Funds

FACTORS AFFECTING TAX ON EQUITY MUTUAL FUNDS

There are multiple factors that affect the Tax Calculation on equity mutual funds listed below:

Dividends

Dividends are the small payments made to your bank account directly, on holding the mutual fund units that pay out dividends. If mutual fund you bought contain some companies that pays out dividends from their earnings or profits, this mutual fund will give you the dividends paid by the company.

Dividend is part of the returns you get from mutual fund and hence need to be added to your annual income and taxed according to income tax slab rates.

Fund Type

Taxation also depends on the fund type you are investing in. For equity mutual funds in which at least 65% of total assets is allocated to equities or stocks, STCG tax is flat 15% where as LTCG tax is 10% on profits above Rs. 1 Lakh in a financial year.

Where as, if you buy Debt mutual fund in which at least 65% of total assets need to be in debt instruments, both STCG and LTCG are taxed based on your income tax slab rates after adding the profits to your annual income.

So mutual fund taxation depends on the fund type you invest in.

Holding Period

In terms of equity mutual fund, the holding period of the units is quite important to calculate tax. More the holding period, less tax will be paid by you on your profits.

That is why for short term profits, you pay flat 15% tax on these gains, where as for long term profits, you pay only 10% tax on these gains that too after Rs. 10 lakh of profits in financial year. Which means, you don’t pay any tax on first Rs. 1 lakh profits in mutual funds in financial year.

Capital Gains

As mentioned above, capital gains are of two types:

- STCG (Short Term Capital Gains) – Holding period is less than 1 year

- LTCG (Long Term Capital Gains) – Holding period is more than 1 year

Longer the time period you hold the mutual funds, lower tax will be paid by you.

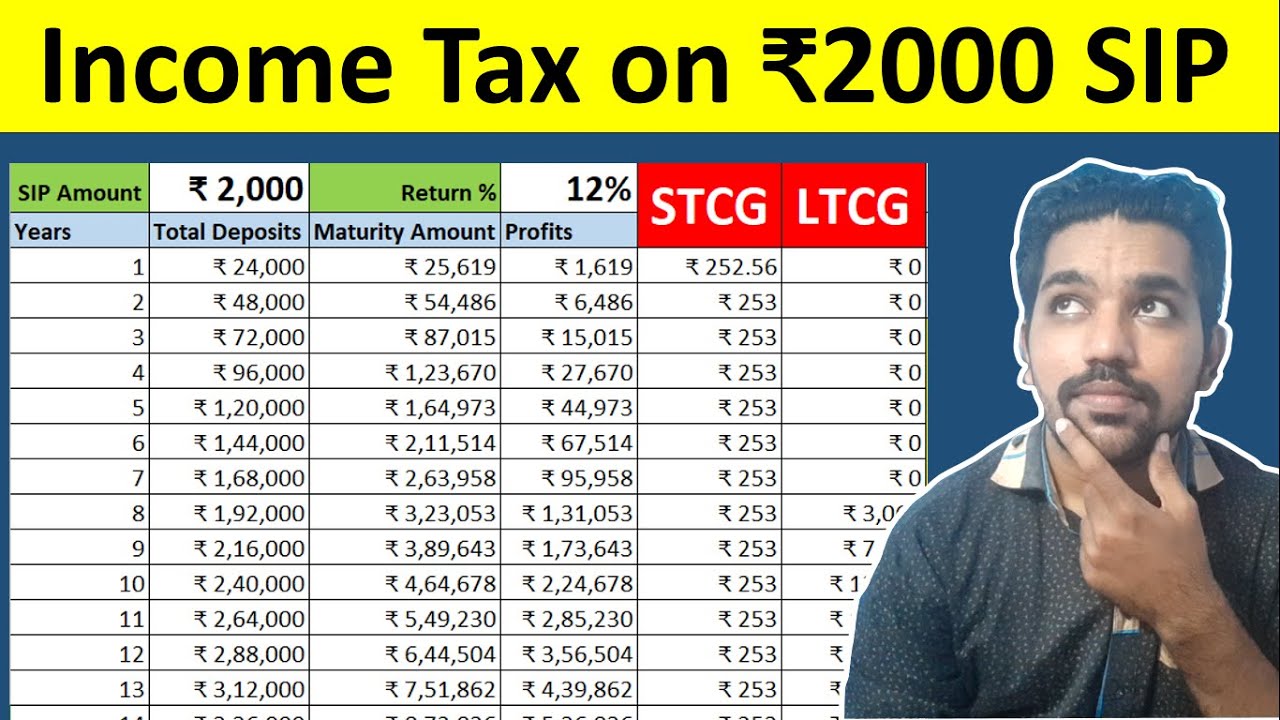

ALSO READ: Rs. 2000 Sensex Returns in last 15 Years

PROFITS ON EQUITY MUTUAL FUNDS

You make profits from equity mutual funds in 2 ways:

- Dividends: These are the periodic small payment made to your bank account if the mutual fund holds some companies that pays out dividends from their earnings / profits to investors. This is possible only when you invest in dividend paying mutual funds. There are other mutual funds which instead of paying you dividends, invest it in more investing opportunities to maximize your capital gains when you redeem mutual fund units.

- Capital Gains: This is the profit you make after selling the mutual fund units on a price higher than the purchase price. For example, if you bought mutual fund units for Rs. 1 Lakh and sell them for Rs. 1.2 Lakh, than you make Rs. 20,000 capital gains or profits.

So these are the two types of profits you make from equity mutual funds, from which, capital gains is the most common type of profit you make after selling the mutual fund units you bought.

Love Reading Books? Here are some of the Best Books you can Read: (WITH LINKS)

TAX RATES ON EQUITY MUTUAL FUNDS

Below are the income tax rates on equity mutual funds:

- STCG (Short term capital gains) Tax Rate: Flat 15% will be the tax you have to pay on profits you make as STCG or short term, which is applicable when you buy and sell mutual fund units within 1 year.

- LTCG (Long Term capital gains) Tax Rate: 10% of tax will be applicable on the profits above Rs. 1 Lakh (in financial year) you make as LTCG or long term, which is applicable when you buy and sell mutual fund units after 1 year.

Let us now understand Equity Mutual Funds Taxation examples.

EQUITY MUTUAL FUNDS TAXATION EXAMPLE

STCG Example

Let’s say you bought mutual fund for Rs. 1 lakh on 1st January 2023, and sell it for Rs. 1.20 Lakh on 1st December 2023. In this case, you make a profit of Rs. 20,000 based on below formula:

Profits = Selling prize - Purchase prize

Profits = Rs. 1,20,000 - Rs. 1,00,000

Profits = Rs. 20,000Now, since the holding period is less than 1 year – between 1st January 2023 to 1st December 2023, the profits made will be termed as Short Term Capital Gains, and will be taxed at flat 15% rate.

So tax on Short term gains will be calculated using below formula:

STCG Tax = Profits * Tax Rate / 100

STCG Tax = Rs. 20,000 * 15 / 100

STCG Tax = Rs. 3000So based on above calculation example, you have to pay Rs. 3000 on the short term profits of Rs. 20,000 you made in this mutual fund.

Let us now understand long term capital gains taxation example on equity mutual funds.

LTCG Example

Let’s say you bought mutual fund units of Rs. 1 Lakh on 1st January 2023 and sell them on 1st March 2025 for Rs. 2.20 Lakh. In this case, you make a profit of Rs. 1,20,000 based on below formula:

Profits = Selling prize - Purchase prize

Profits = Rs. 2,20,000 - Rs. 1,00,000

Profits = Rs. 1,20,000Now, since the holding period is more than 1 year – between 1st January 2023 to 1st March 2025 (approx. 26 months), the profits made will be termed as Long Term Capital Gains, and will be taxed at 10% rate on profits made above Rs. 1 Lakh.

So tax on Long term gains will be calculated using below formula:

LTCG Tax = Profits above Rs. 1 Lakh * Tax Rate / 100

LTCG Tax = Rs. 20,000 * 10 / 100

LTCG Tax = Rs. 2000So based on above calculation example, you have to pay Rs. 2000 on the long term profits of Rs. 1,20,000 you made in this mutual fund.

So as seen in above calculations of equity mutual fund taxation, you pay less tax on more profits you make via long term capital gains compared to short term profits.

So hold your mutual fund units for long term!

SIP REDEMPTION TAXATION EXAMPLE

SIP in equity mutual funds are taxed when you redeem the mutual fund units on first come first serve basis.

So let’s say if you start SIP on 1st January 2023, and continue till 1st January 2024, then you redeem all units on 31st January 2024.

So in this case the first SIP made is held for more than a year, for which LTCG will be considered on the profit made from 1st SIP installment.

Remaining SIP profits will attract short term gains and accordingly will be taxed as per short term capital gains tax rate of 15%.

You can understand more about SIP Redemption Taxation on equity mutual funds by watching below video having calculation examples:

Mutual Funds Taxation via SIP Video

Watch more Videos on YouTube Channel

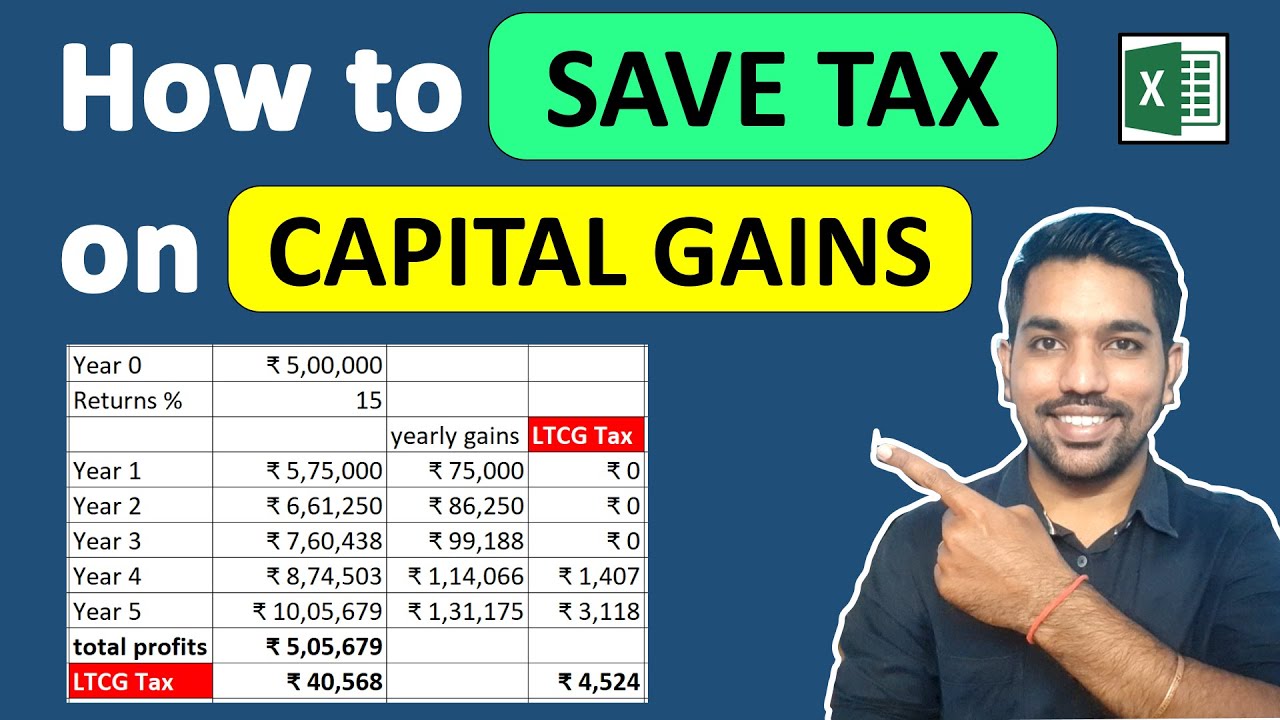

HOW TO SAVE TAX ON EQUITY MUTUAL FUNDS USING TAX HARVESTING?

One of the best ways to save income tax on equity mutual funds is using tax harvesting. Which means, the first Rs. 1 lakh profits you make in a financial year will be tax free, using which one can save tax on mutual funds.

After first year redeem only those units that give profits within Rs. 1 lakh, and repeat this process every year. In this way, you can save tax to some extent while selling the mutual fund units.

Understand this process of tax harvesting in below video:

CONCLUSION

So short term gains are taxed at flat 15% rate and long term gains are taxed at 10% on profits made above Rs. 1 Lakh in financial year. If the holding period is less than 1 year than profits belong to short term capital gains and if the holding period is more than 1 year than profits belong to long term capital gains.

It is best to hold the mutual fund units for long term to reduce tax on profits.

Some more Reading:

- Retirement Planning Calculator in Excel

- SWP for Monthly Income

- SIP vs Lump sum Investments in Mutual Funds

FREQUENTLY ASKED QUESTIONS

Is equity mutual fund tax-free?

No, equity mutual fund profits are not tax free and you need to pay tax on profits you make. For short term gains (holding period less than 1 year), flat 15% tax is applicable on profits, where as for long term gains (holding period more than 1 year) 10% tax is applicable on profits made above Rs. 1 Lakh in financial year.

How is income tax calculated on equity mutual funds?

Income tax is calculated based on the holding period of the equity mutual fund. STCG attracts 15% tax and LTCG attracts 10% tax on profits above Rs. 1 lakh in a financial year.

What is the tax rate for long-term equity mutual funds?

10% of profits made above Rs. 1 Lakh in a financial year

Is dividend from equity mutual fund taxable?

Yes dividends from equity mutual funds are added to your annual income and taxed as per the income tax slab rates.

0 Comments